|

| |

|

|

| |

|

An unusual situation |

|

|

|

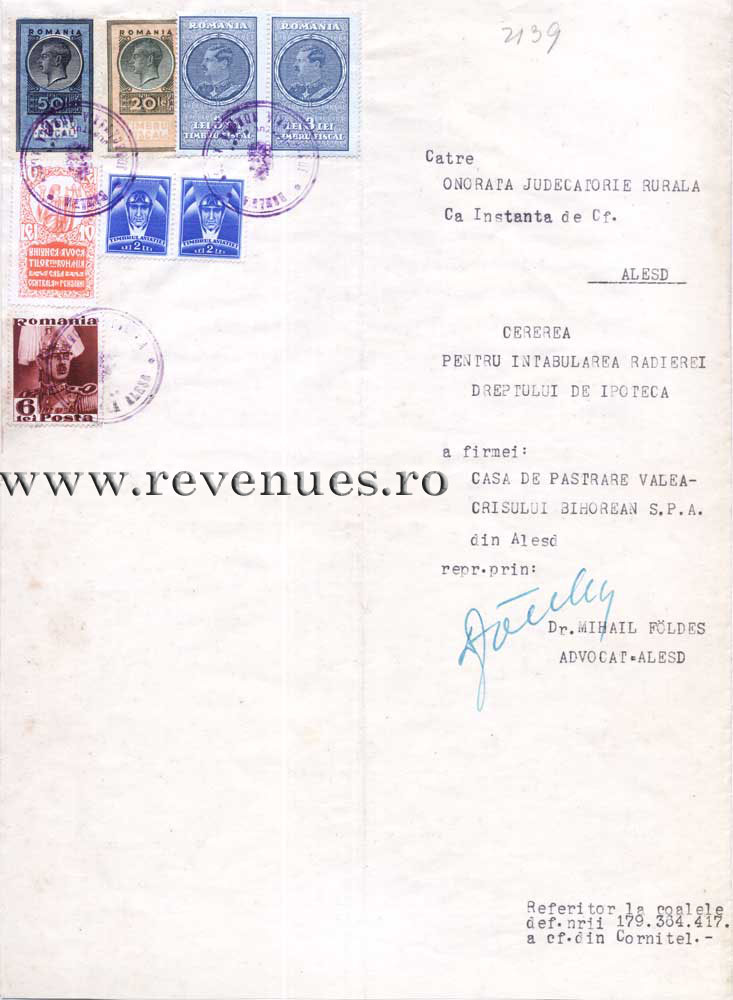

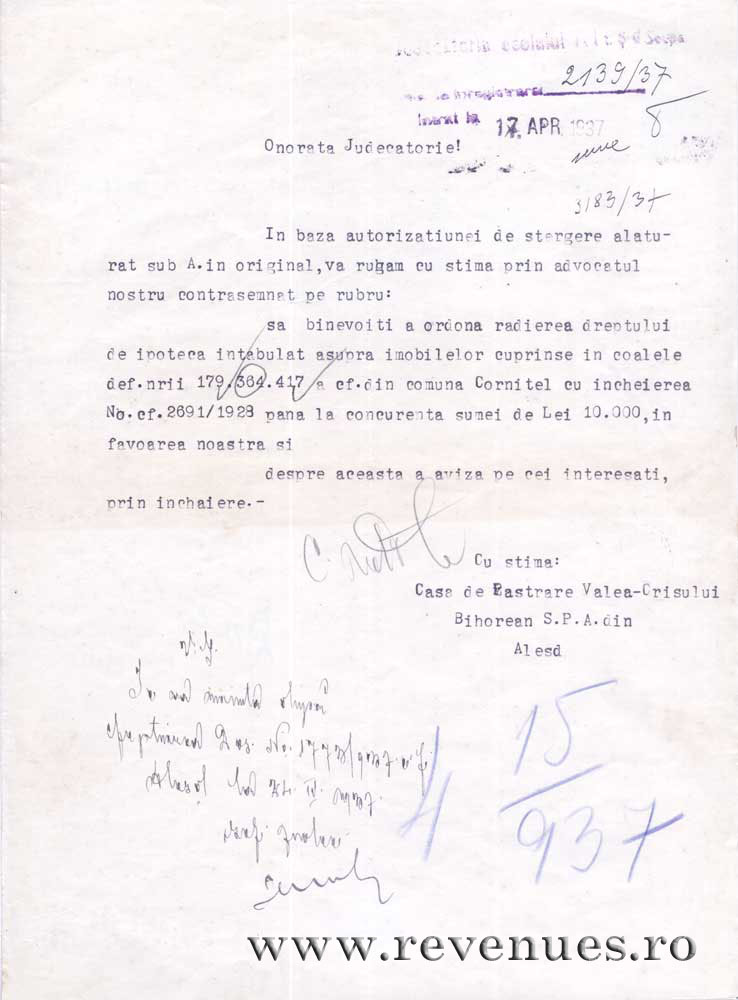

On the document presented (the request to remove a mortgage over some assets, dated 17th of April 1937) was used and canceled a brown postage stamp with the 6 lei value from the 1935 issue named "Carol II uzuale (with word Posta)".

The piece is interesting for both revenue stamp collectors as well as postage stamp collectors from the between wars period.

It is the first piece of this type which I see in almost 40 years of philately, and the fact that from the same period we know of post correspondence stamped with revenue stamps applied next to or instead of postage stamps makes me to believe that it is very rare. All the taxes payd on this document appears to be correct. On the document presented (the request to remove a mortgage over some assets, dated 17th of April 1937) was used and canceled a brown postage stamp with the 6 lei value from the 1935 issue named "Carol II uzuale (with word Posta)".

The piece is interesting for both revenue stamp collectors as well as postage stamp collectors from the between wars period.

It is the first piece of this type which I see in almost 40 years of philately, and the fact that from the same period we know of post correspondence stamped with revenue stamps applied next to or instead of postage stamps makes me to believe that it is very rare. All the taxes payd on this document appears to be correct.  The paid revenue stamp tax in value of 66+8 lei, according to the Stamp and Tax on Documents and Legal Acts Law from the 29th of April 1927, revised, modified and approved in the Official Monitor from 1935, article 4, paragraph 2a. The 10 lei Legal Stamp Tax, established according to the Law for the organization of the lawyers body from the 28th of December 1931 and the Aviation Stamp tax in value of 4 lei, according to the new Law of the National Aviation Fund from the 18th of May 1932 being paid, also according to the habit of the day and at the value established by law. It remains to justify the 6 lei postage stamp. Was it desired to send the document by mail? But then the stamp should not have been applied next to the revenue stamps, but should have been applied separately so as not to create confusions, on another part of the document, as seen on several similar cases, and the stamp should have been a postal stamp and not a tax payer stamp. Could somebody have confused the taxes and stamps which should have been applied? In this case the legal fiscal tax fees were not respected. Questions which request an answer. Without doubts you can affirm that this piece is unusual, worthy of being presented both in postage stamp and revenue stamp catalogues. I make an appeal to collectors to express a point of view on this piece and to present the eventual similar pieces which they know or have in their collections. The paid revenue stamp tax in value of 66+8 lei, according to the Stamp and Tax on Documents and Legal Acts Law from the 29th of April 1927, revised, modified and approved in the Official Monitor from 1935, article 4, paragraph 2a. The 10 lei Legal Stamp Tax, established according to the Law for the organization of the lawyers body from the 28th of December 1931 and the Aviation Stamp tax in value of 4 lei, according to the new Law of the National Aviation Fund from the 18th of May 1932 being paid, also according to the habit of the day and at the value established by law. It remains to justify the 6 lei postage stamp. Was it desired to send the document by mail? But then the stamp should not have been applied next to the revenue stamps, but should have been applied separately so as not to create confusions, on another part of the document, as seen on several similar cases, and the stamp should have been a postal stamp and not a tax payer stamp. Could somebody have confused the taxes and stamps which should have been applied? In this case the legal fiscal tax fees were not respected. Questions which request an answer. Without doubts you can affirm that this piece is unusual, worthy of being presented both in postage stamp and revenue stamp catalogues. I make an appeal to collectors to express a point of view on this piece and to present the eventual similar pieces which they know or have in their collections.

Francisc Ambrus, May 12, 2006

|

|

|

O circulaţie neobişnuită |

|

|

|

În documentul alăturat (cererea unei firme de scoatere din ipotecă a unor bunuri, datată 17 aprilie 1937) a fost utilizată şi anulată o marcă poştală de 6 lei brun din emisiunea din 1935 "Carol II uzuale (cu Poşta)". Piesa este de interes atât pentru colecţionarii de timbre fiscale, cât şi pentru cei de mărci poştale din perioada interbelică. Este prima piesă de acest gen întâlnită de mine în aproape 40 ani de filatelie, iar faptul că din aceeaşi perioadă se cunosc corespondenţe poştale francate cu mărci fiscale aplicate alături sau în locul celor poştale, mă fac să cred că este mult mai rară. Toate taxele achitate pe acest document par să fie corecte. Taxa de timbru fiscal în valoare de 66 + 8 lei achitată, conform Legii Timbrului şi a Impozitului pe Acte şi Fapte Juridice din 29 aprilie 1927 revizuită, modificată şi aprobată ca ediţie oficială la Monitorul Oficial 1935, art.4 paragraful 2a. Taxa de Timbru Judiciar de 10 lei instituită în baza Legii pentru organizarea corpului de avocaţi din 28.12.1931 şi taxa de Timbrul Aviaţiei de 4 lei după noua lege a Fondului Naţional al Aviaţiei din 18.05.1932 fiind achitate, de asemenea, conform uzanţelor vremii şi la tariful prevăzut de lege. Rămâne justificarea mărcii poştale de 6 lei. Să se fi dorit expedierea prin poştă a documentului ?! Atunci timbrul nu-şi avea locul lângă cele fiscale, el trebuind a fi aplicat separat tocmai ca să nu se creeze confuzii, pe altă parte a documentului, aşa cum am mai întâlnit în câteva cazuri asemănătoare, iar ştampila trebuia să fie poştală şi nu a plătitorului de taxe. Să fi confundat cineva taxele şi timbrele ce trebuiesc aplicate ? În acest caz nu s-au mai respectat tarifele fiscale legal percepute. Întrebări ce îşi doresc un răspuns. Fără dubii se poate afirma că această piesă este una deosebită, meritând semnalarea atât în cataloagele de mărci poştale, cât şi în cele de timbre fiscale. Fac un apel la colecţionari să-şi exprime punctul de vedere legat de această piesă şi să semnaleze eventualele piese asemănătoare pe care le cunosc sau le au în colecţie.

Francisc Ambrus, Mai 12, 2006

|

|

|

|

|